Over the past decade, India has witnessed a dramatic transformation in its entrepreneurial landscape. Driven by digitization, policy reforms, and a surge in startup culture, new company incorporations have become a critical indicator of regional economic momentum. This report analyzes incorporation trends across India’s top Tier 1 and Tier 2 cities, based exclusively on Ministry of Corporate Affairs (MCA) data spanning FY2017 to FY2025.

The objective is twofold:

- To decode macro trends, how incorporation activity has evolved year-on-year and quarter-on-quarter, including the impact of macroeconomic cycles, recovery post-COVID, and seasonal behavior.

- To benchmark city-level performance, identifying top-performing cities, underperformers, and emerging hubs within both Tier 1 and Tier 2 segments.

While Tier 1 cities like New Delhi, Mumbai, and Bangalore continue to lead in absolute numbers, Tier 2 cities such as Jaipur, Lucknow, and Ghaziabad are rapidly closing the gap in relative growth. From the FY2023 downturn to the robust resurgence in FY2024–25, both tiers exhibit cyclical but synchronized recovery trends, although the volatility and growth intensity vary between them.

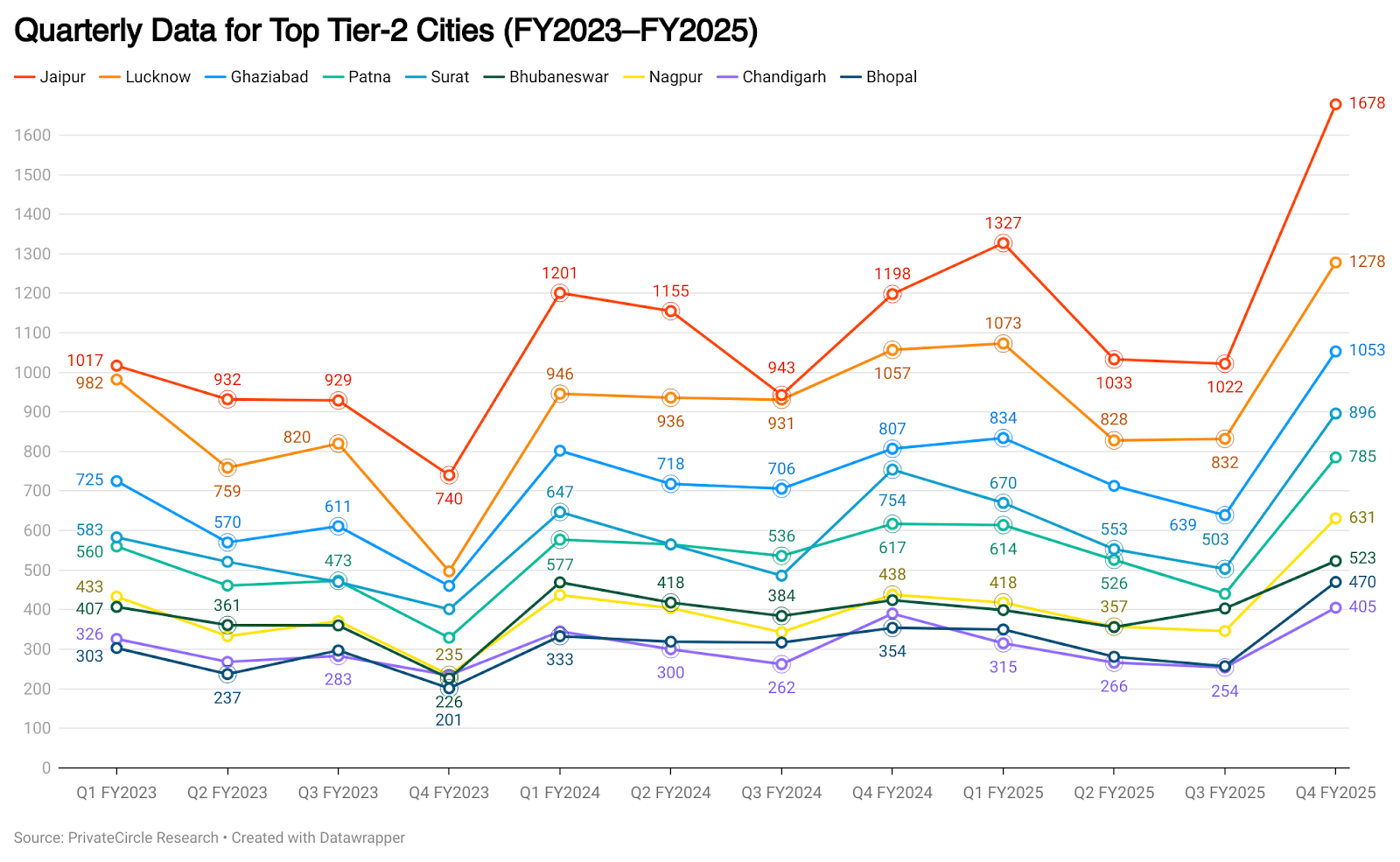

Quarterly Data for Top Tier-2 Cities (FY2023–FY2025)

Tier-2 cities demonstrated a significant revival in business confidence over the three years. Starting from a low of 3,323 incorporations in Q4 FY23, these cities more than doubled their activity to 7,719 incorporations in Q4 FY25. This resurgence reflects a shift in entrepreneurial energy beyond metros, supported by policy initiatives, digital access, and growing regional demand.

The data reveals a seasonal rhythm: every Q4 emerges as the strongest, with spikes likely driven by end-of-year business planning, compliance timelines, and funding cycles. For instance:

- Q3 FY25: 4,696 → Q4 FY25: 7,719 (+64%)

- Q4 FY23: 3,323 → Q1 FY24: 5,757 (+73%)

Jaipur stood out as the Tier-2 frontrunner with 1,678 incorporations in Q4 FY25, followed by Lucknow (1,278) and Ghaziabad (1,053). These cities have consistently led the pack in Tier 2. In contrast, Bhopal (470) and Chandigarh (405) remained on the lower end despite some gains.

The cyclical highs and mid-year lows (Q2, Q3) suggest that incorporations are timed deliberately. While Tier-2 volumes lag behind Tier-1, their rate of growth signals strong latent potential and market maturation.

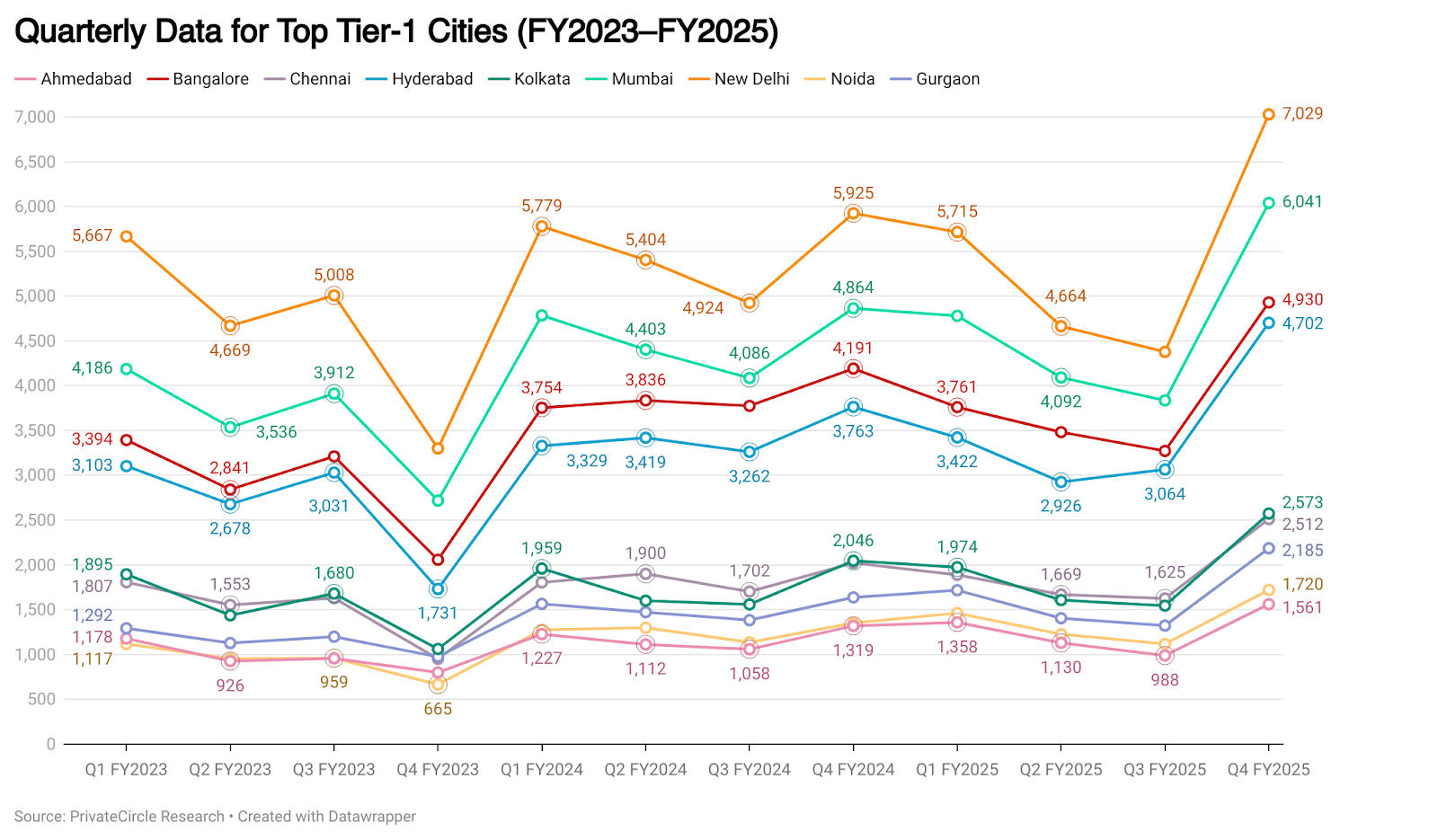

Quarterly Data for Top Tier-1 Cities (FY2023–FY2025)

India’s Tier-1 cities continued to set the pace for company creation. From 14,256 incorporations in Q4 FY23, activity surged to 33,253 by Q4 FY25, a remarkable 2.3x increase. This reflects a macroeconomic rebound, stronger investor appetite, and a mature regulatory environment.

Seasonality remained strong here, too:

- Q3 FY25: 21,148 → Q4 FY25: 33,253 (+57%)

- Q4 FY23: 14,256 → Q1 FY24: 25,477 (+79%)

New Delhi (7,029), Mumbai (6,041), and Bangalore (4,930) were the top-performing cities, together contributing nearly half the Tier-1 incorporations in Q4 FY25. Cities like Ahmedabad (1,561) and Noida (1,720) were lower but still ahead of most Tier-2 peaks.

Even Tier-1’s least active cities surpassed Tier-2 leaders in volume, reflecting their deeper institutional strength and established startup ecosystems. The absolute scale of Tier-1 cities continues to make them the primary engines of formal economic activity.

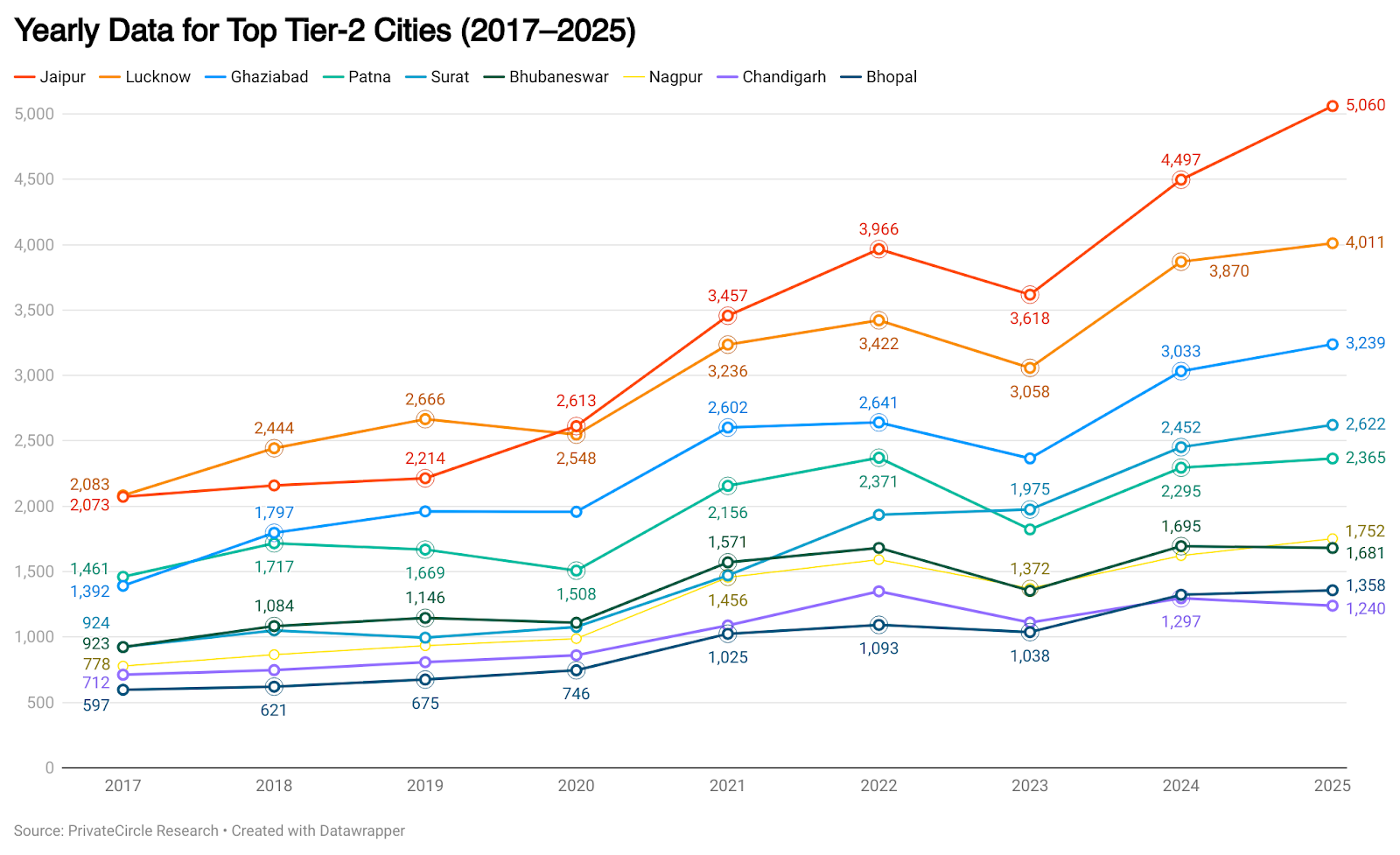

Yearly Data for Top Tier-2 Cities (2017–2025)

Over nine years, Tier-2 cities doubled their formal incorporations, from 10,943 in 2017 to 23,328 in 2025. The rise highlights the steady formalization of India’s regional business landscape.

Two periods stand out:

- 2020 → 2021: +35% growth (13,408 → 18,063), likely driven by post-COVID resilience.

- 2023 → 2024: +25% rebound after a temporary contraction in 2023 (–11.7%).

Jaipur led with 5,060 incorporations in 2025, followed by Lucknow, Ghaziabad, and Surat, cumulatively forming the Tier-2 growth backbone. On the lower side, Bhopal (1,358), Chandigarh (1,240), and Nagpur (1,752) made slower gains.

These trends confirm that Tier-2 cities are no longer passive players. They’re actively building business ecosystems, often aided by state incubation programs and growing digital infrastructure.

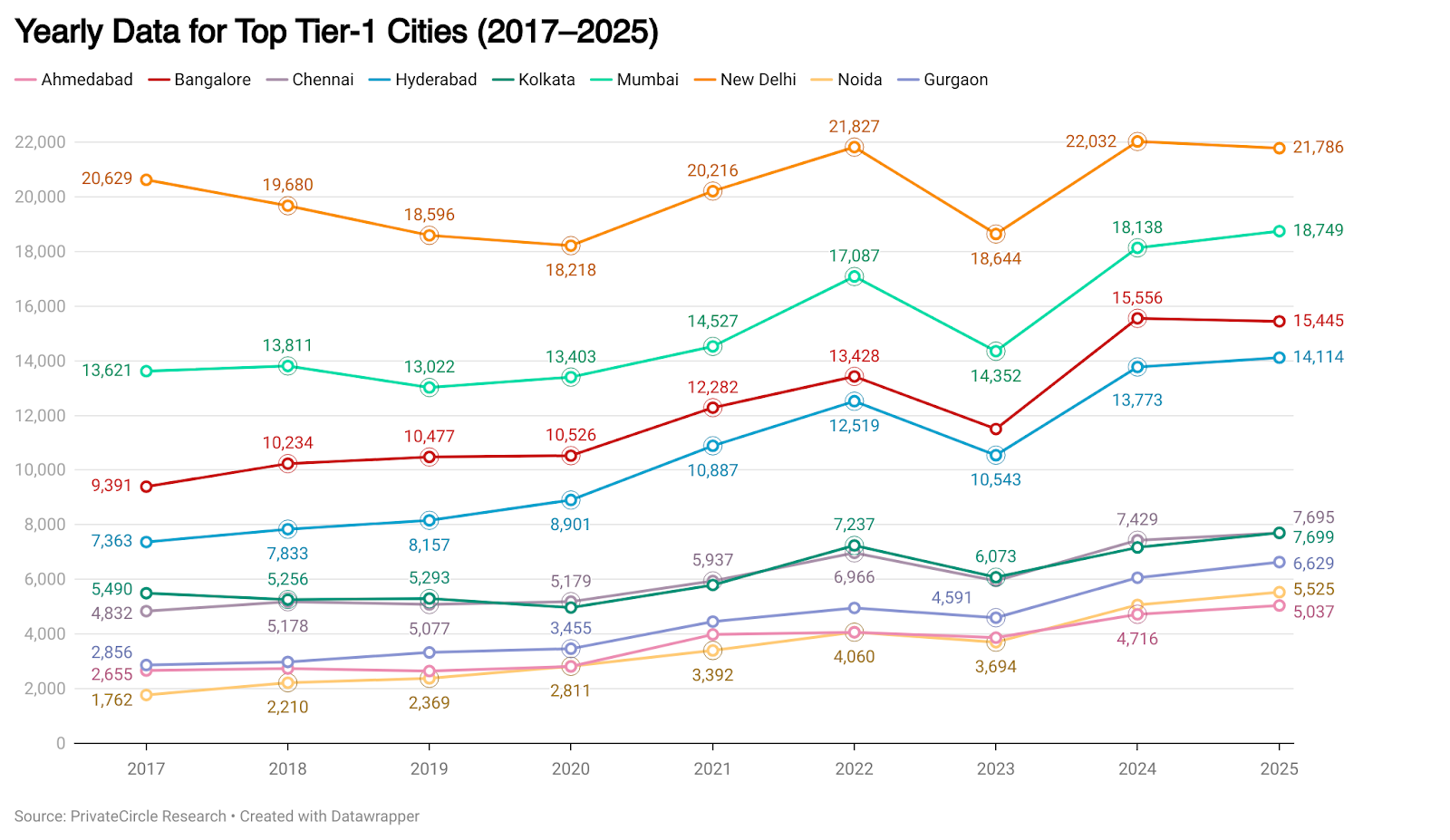

Yearly Data for Top Tier-1 Cities (2017–2025)

Tier-1 cities experienced a textbook recovery cycle. From 68,599 in 2017, incorporations grew to 102,679 in 2025, marking a ~50% increase despite pandemic disruptions.

Key inflection points:

- 2020 → 2021: +15.9% growth amid a startup resurgence

- 2023 → 2024: +26.2% rebound after a major dip

New Delhi (21,786) remained the national leader, contributing over one-fifth of Tier-1 incorporations in 2025. Mumbai (18,749) and Bangalore (15,445) were close behind, demonstrating sustained momentum.

Even smaller Tier-1 cities like Noida (5,525) and Gurgaon (6,629) outpaced major Tier-2 metros. This further underscores the robust institutional and capital frameworks concentrated in India’s primary economic centers.

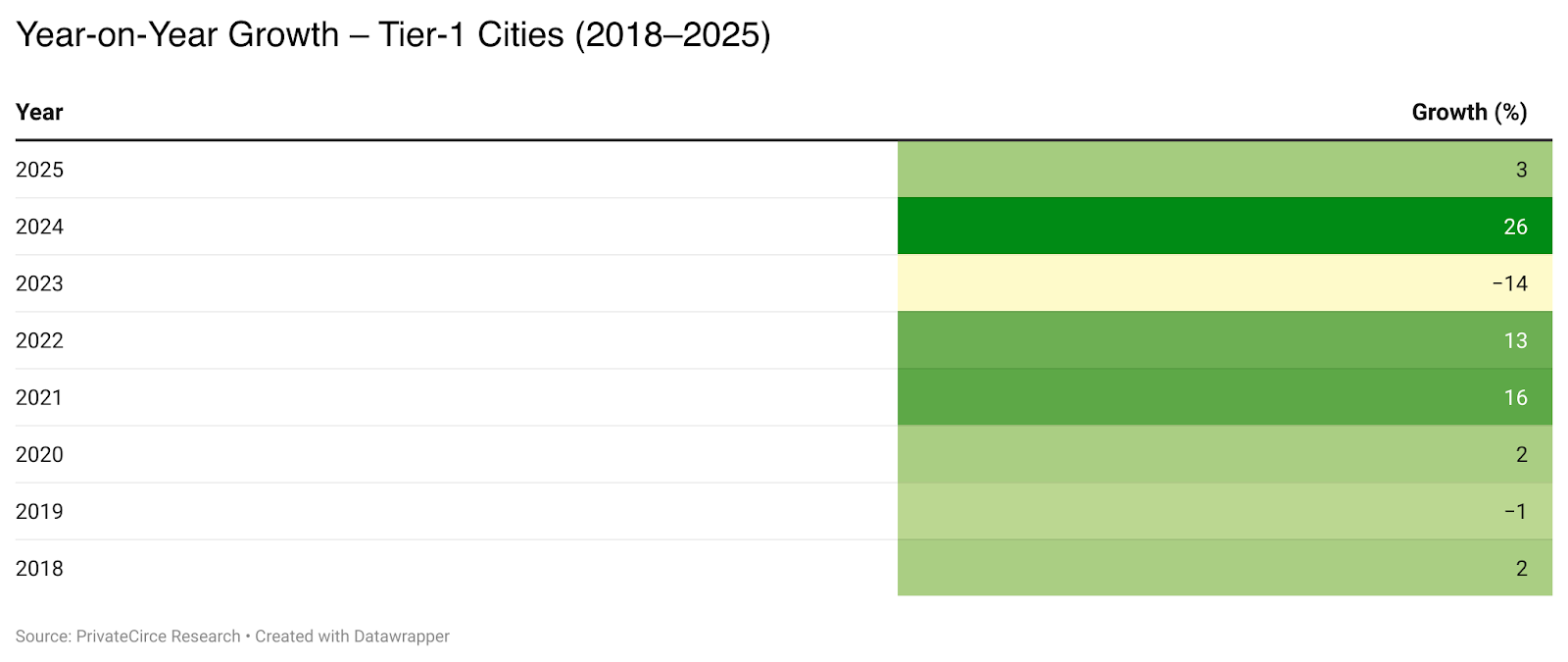

Year-on-Year Growth Tier-1 Cities (2018–2025)

Tier-1 cities saw volatile YoY growth, reflecting sensitivity to macroeconomic shifts:

- 2021: +15.93% rebound after pandemic lows

- 2023: –14.04% contraction amid global uncertainty

- 2024: +26.17% surge, the highest annual jump of the dataset

The post-2020 years show that Tier-1 activity is closely tied to economic cycles, VC sentiment, and policy changes. FY2025’s modest +2.76% suggests consolidation after a massive 2024 uptick.

This volatility is a double-edged sword; Tier-1 cities lead recoveries but also experience sharper slowdowns due to their exposure to institutional trends.

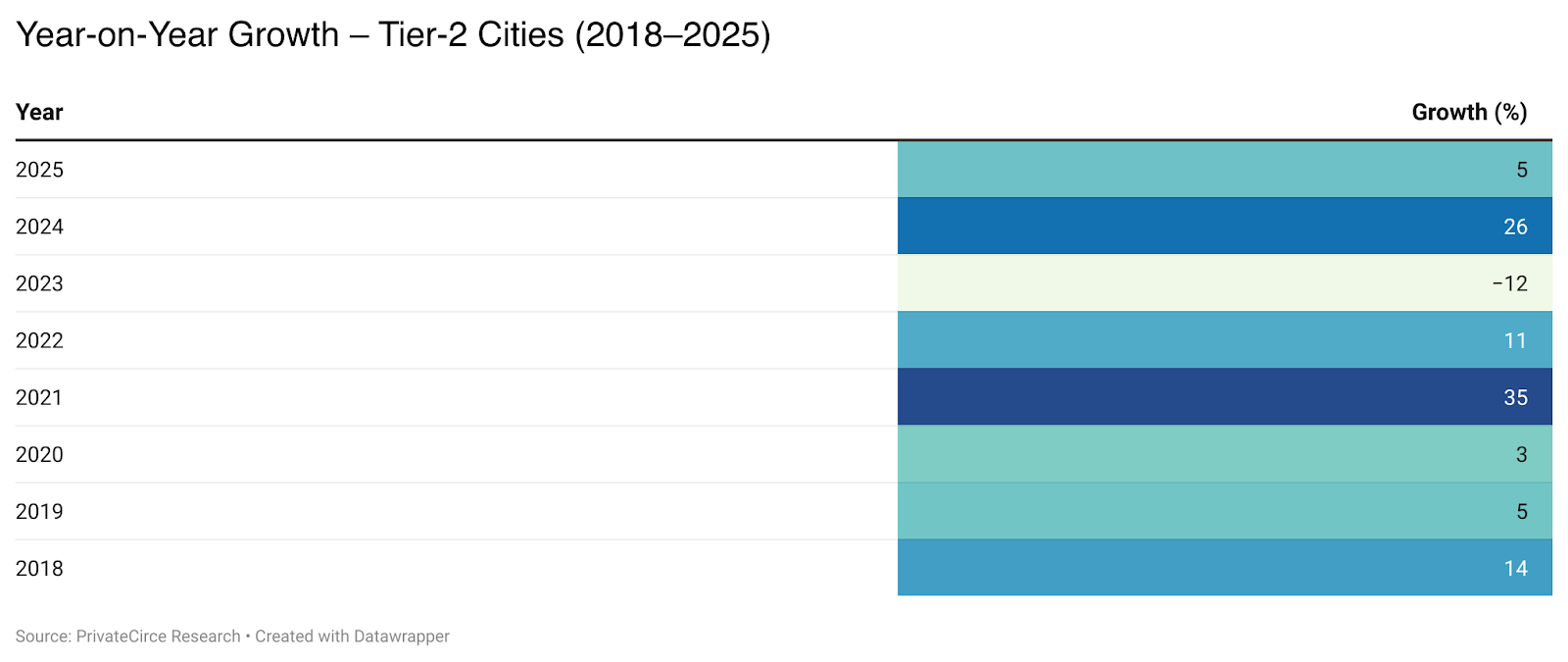

Year-on-Year Growth Tier-2 Cities (2018–2025)

Tier-2 cities displayed even sharper YoY swings, owing to a smaller base and dynamic policy environments:

- 2021: +35.29%, the fastest growth year across both tiers

- 2023: –11.97% , still less severe than Tier-1’s –14.04%

- 2024: +25.62%, strong recovery across the board

Unlike Tier-1, Tier-2 cities experienced more erratic but amplified movements. The high-growth years (2021, 2024) indicate that Tier-2 ecosystems are ripe for scale, while dips tend to be shorter and less extreme.

By FY2025, growth stabilized to +5.39%, potentially pointing to a consolidation phase or regional maturity.

🚀 Startup Support Across India

Tier-2 Cities Are Powering India’s Next Startup Surge

As India’s entrepreneurial landscape matures, the action is no longer confined to metro corridors. Tier-2 and Tier-3 cities are emerging as serious contenders, thanks to a strategic government push and growing private sector participation.

🏛️ Government Initiatives: Taking Startups Beyond the Metros

State governments have realized that nurturing entrepreneurship must go beyond big cities. Their focus is clear: expand startup ecosystems in smaller towns with real incentives.

1. Pan-India Startup Policies

✅ Over 30 Indian states have active startup policies

✅ Common incentives include:

• Seed grants between ₹5–10 lakh for early-stage founders

• Reimbursements on office rent, patent filings, and internet costs

• Tax holidays for 3–5 years to help new startups gain footing

2. Spotlight on Tier-2 Momentum

- Rajasthan (Jaipur): The iStart program has turned Jaipur into a startup magnet by offering funding, mentorship, and incubation right from the seed stage.

- Uttar Pradesh (Lucknow): Under the UP Startup Policy 2020, cities like Kanpur, Meerut, and Prayagraj are seeing incubation centers rise rapidly.

- Tamil Nadu: The Startup & Innovation Policy 2023 sets a goal of 15,000 startups by 2032, with focused efforts in Coimbatore, Madurai, and Tirunelveli.

- Kerala: Through KSUM and infrastructure like the Digital Science Park, cities such as Kochi and Calicut are becoming deep-tech and hardware hubs.

- Jharkhand & Odisha: Startup yatras, seed fund schemes, and digital outreach platforms are now uncovering talent in cities like Ranchi, Rourkela, and Bhubaneswar.

🎯 Impact: As of 2023, nearly 50% of DPIIT-recognized startups now come from Tier-2 and Tier-3 cities, a significant shift from just a few years ago.

🏦 Bank & Private Sector: Unlocking Capital Across Geographies

India’s private financial institutions are now deeply engaged in the startup movement, offering banking, credit, and mentorship services tailored for startups, regardless of location.

1. Startup-Friendly Banking is Here

- SBI Startup Hub (Bengaluru): Offers end-to-end services, from incorporation to IPO advisory, for founders, with more branches planned.

- HDFC, ICICI, IDFC First Bank: All offer startup-focused current accounts with no balance requirements, free transactions, and integrated tools.

- IDFC FIRSTWINGS: Goes a step further with founder mentorship, networking, and co-branded perks for early-stage companies.

2. Credit Where It Counts

- CGSS (Credit Guarantee Scheme for Startups):

🟢 Collateral-free loans up to ₹20 Cr

🟢 85% loan guarantee for smaller-ticket loans, perfect for Tier-2 founders who lack asset backing - Angel & Micro-VC Networks Expanding:

🔹 Jharkhand Angel Network (Ranchi) is funding local startups

🔹 Other Tier-2 hotspots like Surat, Nagpur, Indore, and Jaipur now have regular angel outreach

3. CSR & Incubation Ecosystem Strengthening

- HDFC Bank’s Parivartan Grants: ~₹20 crore annually supports 50+ social-impact startups

- Works through leading incubators like IITs, IIMs, Villgro, with strong outreach in Northeast and Tier-2/3 towns

⚖️ Tier-1 vs Tier-2: A Quick Comparison

| Category | Tier-1 Cities | Tier-2 Cities |

| Ecosystem | Dense networks, established mentors & investors | Expanding through state-backed hubs & incubators |

| Capital Access | High VC interest, metro-centric focus | Government grants, bank credit schemes rising |

| Program Usage | Greater awareness, multiple touchpoints | Growing awareness via Yatras & virtual platforms |

| Mentorship | In-person access to top founders & advisors | Remote mentorship is improving via online incubators |

✨ The New Frontier

Tier-2 cities are no longer just followers; they’re shaping India’s startup future. With capital support, policy clarity, and digital reach, cities like Kanpur, Coimbatore, and Ranchi are now fertile ground for world-class innovation.

💡 Tomorrow’s unicorn may not rise from a glass tower in Bangalore, but from a home office in Bhopal or Bhubaneswar.

Powered by PrivateCircle, your trusted source for private market intelligence and real-time company insights.