In 2008, when most Indian fintechs were still a distant dream, Perfios was quietly laying the foundation for what would become the core digital plumbing of the financial sector. Founded by Debasish Chakraborty and V. R. Govindarajan, Perfios began with a bold but unglamorous vision: to clean, structure, and analyze messy financial data at scale.

Back then, banks and NBFCs struggled with manual processes, unstructured documents, and lengthy loan cycles. Perfios stepped in not with a flashy front-end app, but a powerful backend engine that could extract financial insights in minutes from bank statements, ITRs, and PDFs.

Over the years, Perfios became the invisible layer behind India’s lending boom, enabling everything from income analysis and KYC to fraud detection and underwriting. While others chased headlines, Perfios built deep, defensible infrastructure that powered the rise of retail and SME credit.

Today, with more than 1,000 enterprise clients across 18 countries, Perfios is no longer just a backend specialist. It’s a full-stack fintech enabler, ready for the spotlight.

What Perfios Does

Often referred to as the “AWS of fintech underwriting,” Perfios provides critical digital infrastructure for banks, NBFCs, insurers, and fintechs. It doesn’t lend, it enables lending.

At the heart of Perfios’ offerings is a powerful suite of API-led tools for:

- Income analysis (via its Income Analyzer)

- Creditworthiness scoring (via FinScore)

- Digital KYC and onboarding

- Fraud detection

- Document parsing and financial data extraction

These tools are deeply embedded into the workflows of 1,000+ institutions, from large banks to early-stage fintechs, making Perfios the invisible, indispensable layer of modern lending.

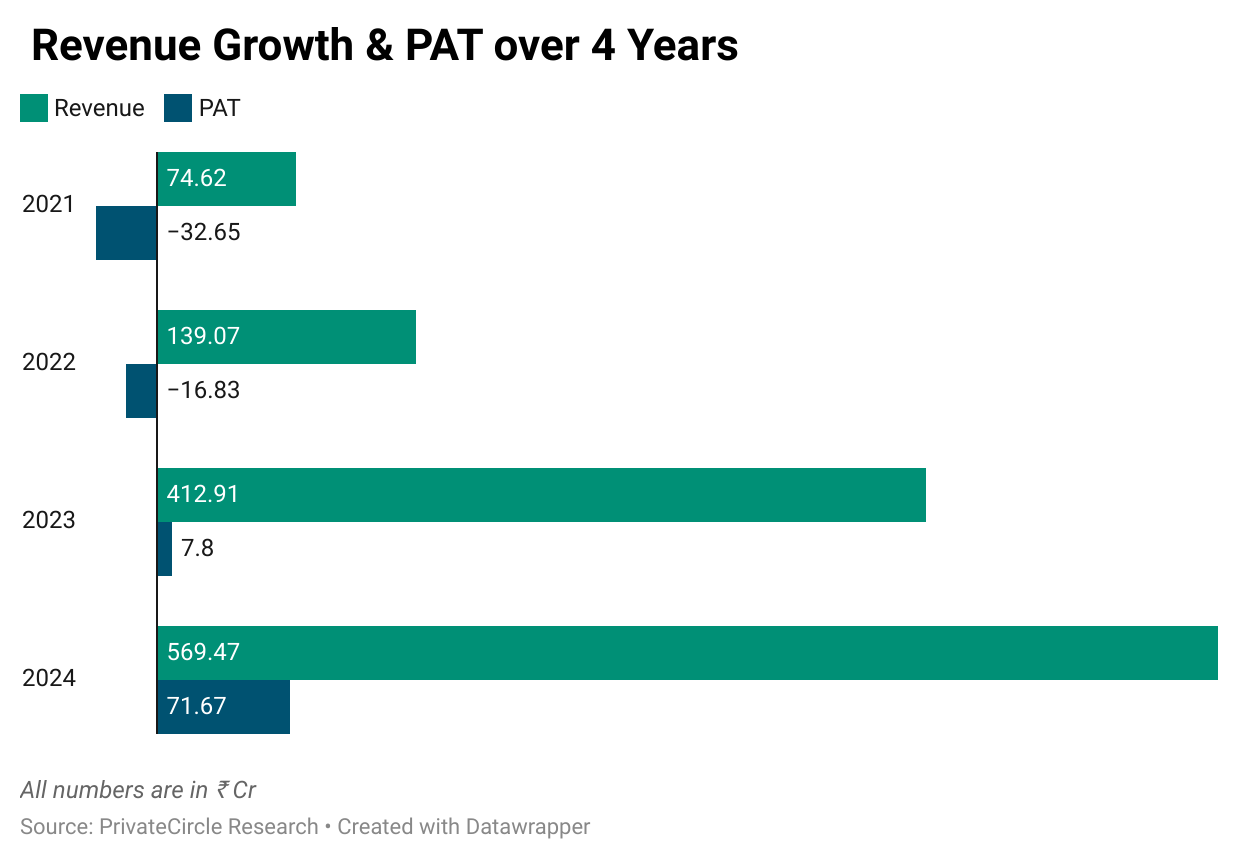

Inside the Books: Perfios’ Revenue & Profit Trajectory (In Cr)

Key Insights on Perfios Financials

1. Revenue Growth Momentum

- 3-Year CAGR (FY21–FY24): ~94.1%

- Perfios has grown 7.6x in revenue from FY21 to FY24 (₹74.62 Cr → ₹569.47 Cr), indicating strong enterprise demand for its fintech infrastructure solutions.

- The steep jump from ₹139 Cr in FY22 to ₹413 Cr in FY23 reflects either new large client wins or expanded product usage across existing customers.

2. PAT Turnaround

- FY21 & FY22 Losses: The company posted losses of ₹32.65 Cr and ₹16.83 Cr, likely due to product development, market expansion, and R&D investments.

- FY23 Break-Even: Achieving ₹7.8 Cr PAT after years of losses marks a critical inflection point, operating leverage kicked in as fixed costs were absorbed over a larger revenue base.

- FY24 Profit Surge: PAT jumped to ₹71.67 Cr, nearly 9x growth YoY, indicating strong margins, cost efficiency, and likely price realization improvements.

3. Scalability & Operating Leverage

- The fact that revenue grew ~38% from FY23 to FY24 while PAT grew ~818% suggests:

- Minimal increase in incremental costs

- High-margin SaaS-style licensing or data monetization

- Strong product-market fit and customer retention

- Minimal increase in incremental costs

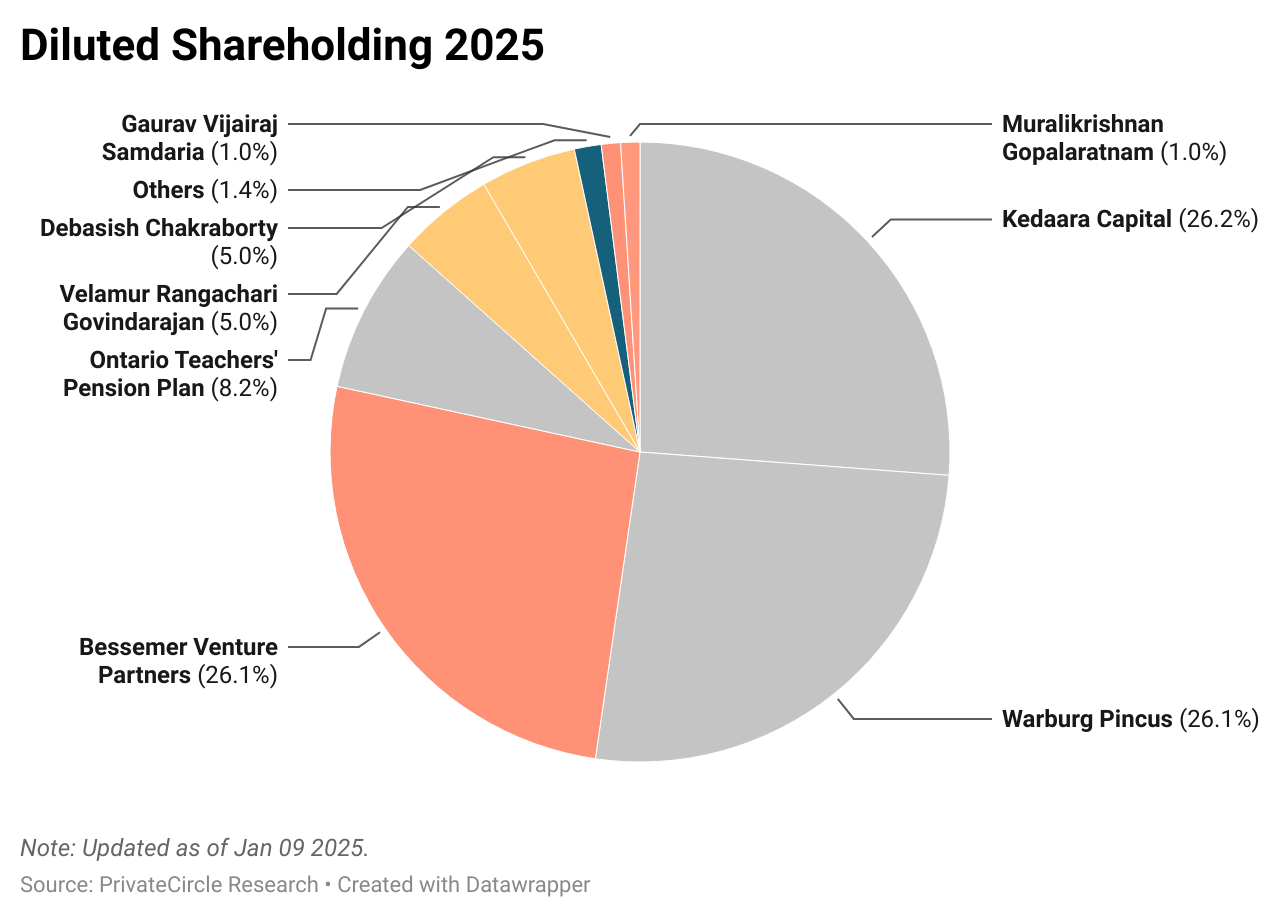

Cap Table: Institutional Muscle Behind Perfios

Perfios’ cap table reflects deep institutional trust:

Perfios isn’t just another fintech IPO; its cap table is a masterclass in institutional confidence:

Perfios’ cap table reflects deep-rooted institutional trust, with three marquee investors, Kedaara Capital, Warburg Pincus, and Bessemer Venture Partners, each holding over 26%, signaling high alignment and a well-balanced governance structure. The presence of the Ontario Teachers’ Pension Plan with an 8.2% stake adds global credibility, showcasing confidence from one of the world’s largest long-term capital allocators. Meanwhile, co-founders Velamur Govindarajan and Debasish Chakraborty continue to hold 5% each, reinforcing strong founder skin in the game. With no single dominant shareholder, Perfios enters the public market with a clean, disciplined, and IPO-ready cap table.

Clientele & Partnerships: Trusted by India’s Financial Backbone

Perfios is deeply embedded in India’s financial infrastructure, powering over 400 financial institutions (FIs) with its API-led solutions for underwriting, credit decision-making, and compliance. Its client list includes marquee names such as ICICI Bank, HDFC Bank, Axis Bank, SBI, Bajaj Finserv, Kotak Mahindra Bank, and Aditya Birla Capital, among others. These institutions rely on Perfios to automate income verification, fraud detection, KYC, and credit analysis, cutting processing time from days to minutes. Beyond banks and NBFCs, Perfios also works with fintechs, insurance companies, and global lenders, acting as the core decision-making engine within their tech stacks. It is also tightly integrated with key regulatory platforms, including the RBI’s Account Aggregator (AA) framework, UIDAI for Aadhaar-based verification, GSTN and ITR data sources, and SIDBI for MSME lending support. These integrations make Perfios not just a tech provider but a trusted compliance-grade partner in India’s evolving digital finance ecosystem.

Key Strengths of Perfios

Deep Domain Moat in Financial Data

Perfios has built a decade-long moat in parsing, analyzing, and interpreting complex financial documents such as bank statements, ITRs, GST filings, and cash flow records. Its proprietary algorithms are trained on over 1.5 billion documents, giving it unparalleled accuracy in financial profiling. This domain expertise makes it hard for new entrants to match its scale or accuracy.

Embedded into Client Workflows (High Stickiness)

Perfios’ APIs are deeply integrated into the loan origination systems (LOS), credit underwriting, KYC, and income assessment processes of over 500+ banks, NBFCs, and fintechs. Once embedded, these APIs become mission-critical, leading to high client retention and recurring revenues. This embedded nature ensures low churn and high lifetime value per customer.

Modular Product Suite (Plug-and-Play APIs)

From KYC automation and income analysis to fraud detection and GST verification, Perfios offers more than 75+ APIs that clients can integrate as per their workflow needs. This modular architecture ensures that both traditional banks and new-age fintechs can use Perfios’ services with minimal friction, making it scalable across sectors and geographies.

Trusted by Leading BFSI Institutions

Perfios powers the backend of credit decisions for India’s largest private banks (like HDFC Bank, Axis Bank), top NBFCs (Bajaj Finance, Tata Capital), and leading fintechs (like Groww, KreditBee, and Slice). The brand’s credibility in managing sensitive financial data at scale makes it a default choice for regulated entities looking for robust credit intelligence infrastructure.

International Expansion & GTM Playbook

Perfios has steadily expanded its footprint beyond India, with a growing presence in key international markets across the Middle East and Africa (MEA) and Southeast Asia (SEA), particularly in countries like Indonesia, the UAE, and Vietnam. Its go-to-market (GTM) strategy follows a partner-first model, collaborating with local financial institutions, fintechs, and system integrators to accelerate adoption and build trust. Recognizing the nuances of each market, Perfios customizes its solutions to meet local regulatory requirements, such as aligning with OJK (Otoritas Jasa Keuangan) regulations in Indonesia. This localization-first approach not only ensures compliance but also strengthens Perfios’ positioning as a global enabler of digital lending and financial infrastructure.

Tech & IP Moat

Perfios has built a strong technology and IP moat centered around its proprietary AI/ML capabilities, purpose-built for the complexities of financial data. At its core are homegrown machine learning models that can intelligently classify, clean, and analyze diverse financial documents, from bank statements and ITRs to GST filings and salary slips. One of its standout innovations is an advanced OCR and AI-powered parsing engine that can extract structured insights from unstructured formats like PDFs, scanned images, and handwritten forms, crucial for onboarding in India and other document-heavy markets. Unlike off-the-shelf scoring tools, Perfios embeds its real-time credit scoring engines directly into client workflows, making its tech mission-critical and non-substitutable. Importantly, the company continues to deepen this moat with sustained R&D investment from its recent Series D funding, allowing it to stay ahead in automation, explainable AI, and regulatory-grade compliance, all tailored specifically for BFSI use cases.

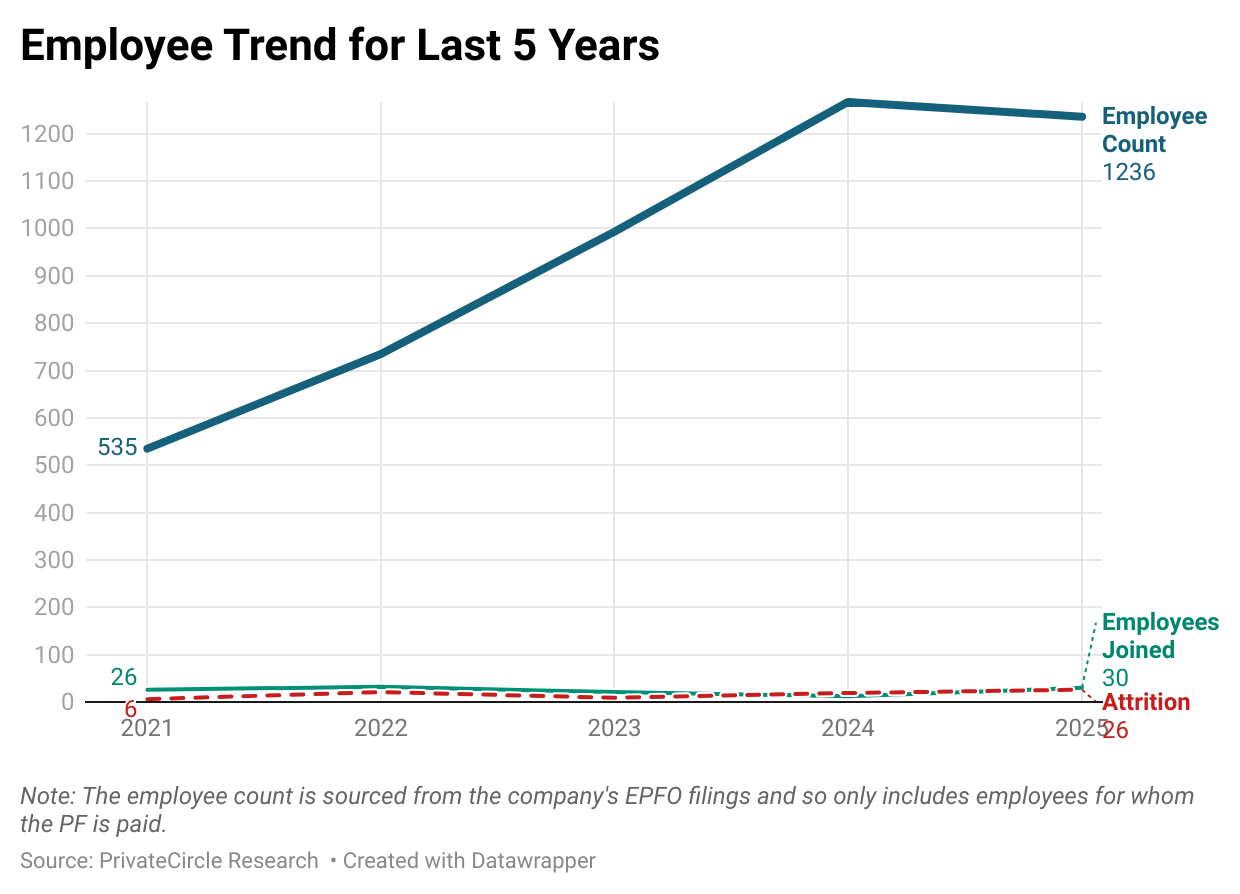

Team @ Scale

Perfios is not just growing revenues, it’s scaling talent too.

Between FY21 and FY25, Perfios scaled its team from 535 to a peak of 1,267 in FY24 before slightly declining to 1,236 in FY25, reflecting a phase of consolidation after rapid growth. While the company aggressively expanded between FY21–FY23, adding over 450 employees, the pace of new hires slowed significantly in FY24 and FY25, with only 12 and 30 joiners, respectively. At the same time, attrition rose, from just 6 in FY21 to 26 in FY25, indicating growing internal churn amid a more mature phase of operations. This trend suggests that while Perfios has stabilized its workforce size, it is now focused on optimizing team quality and managing retention in a scaling organization.

Fintech/Enterprise Infra Comparison: Perfios vs Others

| Metric | Perfios | Innovaccer | Gramener | Lumiq | Sapience |

| Core Product | Credit Infra (APIs, KYC, income analysis) | Health data infra & analytics | Enterprise data storytelling & dashboards | Data infra for BFSI (AI/ML ops) | Workforce analytics & productivity |

| FY24 Revenue (₹ Cr) | 569.47 | 354.2 | 99.88 | 70.53 | 54.54 |

| Global Expansion | Yes (MEA, SEA) | Yes (US-focused) | Yes (India, US, UK, Singapore) | Yes (Middle East, US) | Yes (US + India) |

| Profitability | Profitable | Profitable | Losses | Losses | Profitable |

| IPO-Ready | Yes (DRHP not yet filed) | No | No | No | No |

Observations:

Perfios emerges as the frontrunner in the fintech/enterprise infra space with the highest FY24 revenue at ₹569.47 Cr, solid profitability, and active global expansion across MEA and SEA. While it hasn’t filed its DRHP yet, its IPO readiness reflects strong internal preparedness and investor confidence. Innovaccer ranks second in revenue (₹354.2 Cr) and is also profitable, but its focus remains largely on US healthcare analytics. Gramener and Lumiq, though present in global markets, are loss-making and operate at a smaller scale, indicating early-stage growth or niche positioning. Sapience, focused on workforce productivity analytics, is profitable and globally active but remains the smallest player by revenue. Overall, Perfios leads on all key fronts, scale, profitability, market diversification, and public market potential, making it the most mature and strategically placed among its peers.

What Makes Perfios IPO-Ready

Perfios is primed for the public markets with a rare combination of scale, stability, and global ambition. With FY24 revenue at ₹569.47 Cr and a solid ₹71.67 Cr in profit, the company has demonstrated strong financial discipline while embedding itself in over 400 financial institutions. Its cap table features marquee investors like Warburg Pincus, Kedaara, Bessemer, and OTPP, signaling deep institutional trust. International expansion across Southeast Asia and the Middle East, proprietary AI-driven underwriting tech, and sticky APIs that power everything from KYC to credit scoring have positioned Perfios as a vital layer in the fintech stack. With IPO proceeds earmarked for product innovation, M&A, and global scale-up, the company is stepping into the spotlight with a growth-ready, investor-friendly narrative.

Conclusion: Perfios Is Built for the Big League

In the fast-evolving world of digital finance, infrastructure players rarely make headlines, but Perfios is changing that. Over the past few years, it has become the quiet engine powering India’s lending ecosystem, enabling banks, NBFCs, fintechs, and even global financial institutions to make faster, data-driven decisions. From automated KYC and income analysis to real-time financial APIs, Perfios has built an indispensable layer of credit intelligence for the industry.

Its FY24 performance, ₹569 Cr in revenue with profitability, proves that it’s not only growing fast but growing right. Unlike many enterprise SaaS peers still chasing scale or struggling with losses, Perfios has already crossed key milestones: sustainable operations, global presence across MEA and SEA, and strong client stickiness in a regulatory-heavy environment.

While it hasn’t yet filed its DRHP, the company has signaled clear IPO intent and is widely considered one of the most IPO-ready fintech infra players in the country. As India’s lending ecosystem gets deeper, more digital, and more data-driven, the role of companies like Perfios becomes even more critical.

Perfios isn’t just another SaaS company. It’s a category creator, a market stabilizer, and a potential bellwether for India’s next wave of fintech IPOs. All it needs now is the bell to ring.

🔍 Power your insights with PrivateCircle, India’s most trusted platform for verified startup financials, debt data, and private market intelligen