India’s fintech ecosystem is evolving, and at the heart of this transformation lies a new breed of digital banks targeting the country’s 60 million+ small businesses and self-employed professionals. These are the SME neo-banks, lean, tech-driven platforms aiming to democratize access to financial services in one of the most underserved segments of the economy.

Among them, Chqbook and Instantpay have emerged as two promising, yet fundamentally different, contenders. InstantPay, once known for its utility payments and cash deposit services, has grown into a robust B2B2C infrastructure player, powering over 10,000+ banking touchpoints across India. Its model is API-first, scale-oriented, and heavily focused on digitizing last-mile transactions.

On the other hand, Chqbook is taking a more focused approach, building a full-stack digital banking experience for India’s small business owners, gig workers, and kirana stores. With its mobile-first platform, Chqbook bundles current accounts, working capital loans, insurance, and credit cards into a single user journey tailored for the self-employed.

Both startups are unlisted and currently loss-making. But while they share a common mission, to serve India’s vast informal economy, their strategies, product philosophies, and growth levers differ drastically. This report delves deeply into both companies, exploring their financial performance, business models, customer focus, monetization strategies, and path to profitability. As India’s digital banking space gets more crowded and competitive, the big question is:

Which of these two neo-banks is better positioned to lead the SME fintech revolution?

Company Overview

| Metric | Chqbook | InstantPay |

| Year Founded | 2016 | 2010 |

| HQ Location | Gurgaon | New Delhi |

| Founders | Vipul Sharma, Rajat Kumar, Mohit Goel | Shailendra Agarwal, Amol Sonbarse, Ajay Upadhyay |

| Business Model | App-based digital platform for small business owners | Full-stack open banking infrastructure |

| Target Audience | Kirana store owners, gig economy workers | SMEs, corporates, and government clients |

| Tech Focus | Mobile-first, vernacular support, credit underwriting | API-first, high-volume transactional architecture |

| Go-To-Market Strategy | Agent-assisted onboarding + mobile app | B2B sales, integrations with ERPs, and platforms |

Chqbook follows a distribution-led model, aiming to serve India’s financially excluded micro-entrepreneurs. It provides digital current accounts, loan access, and insurance on a multilingual platform.

InstantPay operates an infrastructure-first model, offering plug-and-play APIs to enterprises, banks, and NBFCs for seamless neo-banking functions. It acts as a digital banking layer over traditional rails.

📊 FY24 Financial Snapshot (₹ Cr)

| Metric | Chqbook | Instantpay |

| Revenue | 11.99 | 77.46 |

| EBIDTA | -21.37 | -1.45 |

| PAT | -25.54 | -2.94 |

| 2 Yr CAGR% | -3.4% | -14.38% |

| 3 Yr CAGR% | 4.54% | -29.28% |

Key Insights: Chqbook vs Instantpay

- Revenue: Instantpay (₹77.46 Cr) significantly outpaces Chqbook (₹11.99 Cr), indicating a larger scale of operations.

- EBITDA: Both are loss-making, but Instantpay’s EBITDA loss (₹1.45 Cr) is far narrower than Chqbook’s heavy loss of ₹21.37 Cr, pointing to better cost efficiency.

- PAT: Chqbook’s PAT loss (₹25.54 Cr) is nearly 9x that of Instantpay (₹2.94 Cr), highlighting profitability challenges.

- Growth Trends:

- Chqbook is showing modest recovery with a positive 3-year CAGR (+4.54%), while Instantpay is sharply declining (-29.28%).

- Over 2 years, both are negative – Instantpay at -14.38%, and Chqbook at -3.4%, with Chqbook showing relatively better resilience.

- Chqbook is showing modest recovery with a positive 3-year CAGR (+4.54%), while Instantpay is sharply declining (-29.28%).

💡 Interpretation: Despite Instantpay’s stronger revenue base, Chqbook’s recent recovery trend (positive 3Y CAGR) could be a green shoot if unit economics improve. However, its high EBITDA and PAT losses remain a concern for long-term sustainability.

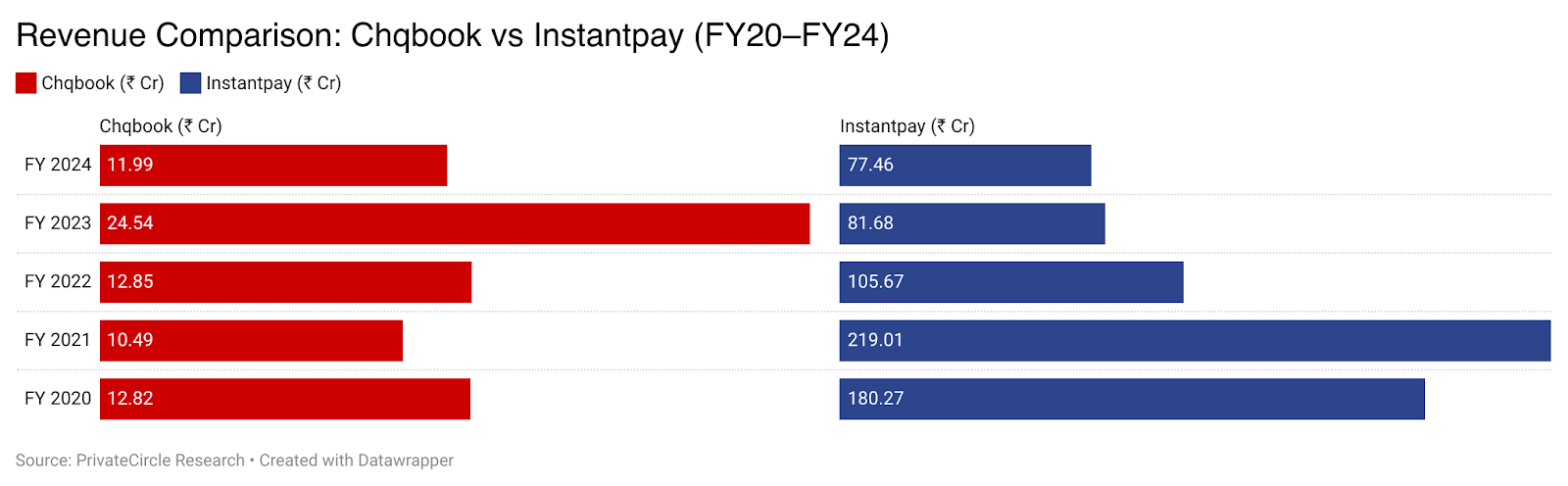

Revenue Comparison: Chqbook vs Instantpay (FY20–FY24)

🔍 Key Insights

- Instantpay peaked in FY21 with ₹219 Cr in revenue but has seen a gradual decline since then, possibly due to market saturation, changes in strategy, or pricing pressure.

- Chqbook, though significantly smaller in size, displayed growth momentum in FY23, nearly doubling revenue, but the FY24 dip suggests ongoing experimentation and customer acquisition challenges.

- Over the last 5 years, Instantpay has consistently maintained higher revenues, reflecting broader market reach and stronger infrastructure partnerships.

- In contrast, Chqbook’s revenues stayed under ₹25 Cr, indicating a niche approach but also highlighting the potential for scale as product-market fit is optimized.

📊 Key Financial Ratio Insights- FY24 (Chqbook vs Instantpay)

| Ratio | Chqbook | Instantpay |

| Quick Ratio | 0.2 | 0.8 |

| Absolute Liquid Ratio | 0.1 | 0.8 |

| Debt Collection Ratio (Receivable Days) | 23 | 20 |

| Fixed Assets Turnover Ratio | 1.31 | 20.08 |

| Asset Turnover Ratio | 0.33 | 1.07 |

🔍 Key Takeaways & Insights

🧊 Liquidity Position

- Instantpay is in a much stronger liquidity position than Chqbook, with a Quick Ratio of 0.8 (vs. 0.2) and Absolute Liquid Ratio of 0.8 (vs. 0.1).

- This means Instantpay has significantly higher immediately available assets to cover short-term liabilities, reducing solvency risk.

- Chqbook’s extremely low ratios suggest high dependency on current receivables or delayed payments to settle dues, raising red flags for working capital stress.

⏱️ Receivables Management

- Both companies have relatively efficient collections, with Instantpay slightly better (20 days vs. Chqbook’s 23 days).

- This indicates Instantpay may have slightly tighter credit control policies or faster payment cycles.

🏭 Operational Efficiency

- Fixed Asset Turnover shows a stark contrast: Instantpay’s 20.08x vs Chqbook’s 1.31x, meaning Instantpay is generating far more revenue from its fixed assets.

- Chqbook’s low ratio implies underutilized or inefficient asset deployment.

📦 Asset Utilization

- Asset Turnover Ratio further confirms this pattern: Instant pay at 1.07 vs Chqbook’s 0.33.

- Instantpay uses its entire asset base 3x more efficiently to generate revenue compared to Chqbook, indicating a leaner, more optimized operations setup.

🧩 SWOT Comparison — Chqbook vs Instantpay

Strengths:

Chqbook has built a strong value proposition for India’s self-employed ecosystem by bundling financial products like loans, credit cards, and insurance into a mobile-first neobank tailored to kirana stores and micro-entrepreneurs. Its recognition through awards like Tech30 and its curated marketplace model have helped it build initial traction, especially among underserved urban users.

Instantpay, on the other hand, is a distribution-led fintech. It has scaled revenue much faster historically, riding on a robust B2B2C infrastructure that powers everything from utility payments and money transfers to API-led banking services. With a peak revenue of ₹219 Cr in FY21, it has demonstrated the ability to operate at large volumes.

Weaknesses:

Chqbook’s financial journey has seen fluctuations, with strong momentum in FY23 followed by a revenue dip to ₹11.99 Cr in FY24. While losses remain high, with PAT at ₹-25.5 Cr, the company is still in the investment phase, focusing on building a comprehensive SME-focused financial platform. The current financial strain, including a negative net worth, underscores the need for strategic capital infusion and tighter cost controls, but does not diminish its long-term market potential.

Instantpay, with a more stable revenue base of ₹77.5 Cr in FY24, has shown resilience despite a downward topline trend since its FY21 peak. While it remains in the red on EBITDA and PAT, its losses are relatively modest compared to peers. The company’s diversified revenue streams and scalable infrastructure position it well to bounce back as demand for API-led banking solutions accelerates.

Opportunities:

Chqbook is well-positioned to tap into India’s growing appetite for formalized credit and financial services among small businesses, especially in Tier 2/3 cities. With the right funding and focus, its personalized offerings and mobile-based distribution can scale rapidly in semi-urban markets.

Instantpay stands to benefit from the boom in embedded finance and B2B API-led platforms. As more enterprises seek to offer banking services natively within their apps, Instantpay’s backend-first model makes it a natural partner for fintechs, logistics firms, and digital-first brands.

Threats:

Chqbook’s capital-heavy losses and declining revenues could make it difficult to sustain investor interest unless it course-corrects quickly. It also faces regulatory uncertainty in areas like digital lending partnerships and FLDG models, which form the backbone of its neobanking model.

Instantpay, while financially more stable, could lose ground to better-funded competitors in the API and BaaS space. Players like RazorpayX, Setu, and traditional banks launching open APIs could commoditize the infrastructure space, putting downward pressure on margins and forcing differentiation through value-added services.

💻 Technology & Innovation Focus — Chqbook vs Instantpay

🔷 Chqbook

- Mobile-first neobank platform tailored for India’s self-employed segment (kiranas, gig workers).

- Offers a unified app experience combining credit, insurance, accounts, and rewards.

- Leverages alternate data (like GST filings, transaction history) for credit underwriting — enabling loans for thin-file customers.

- Designed for vernacular and multilingual onboarding, making it accessible across Bharat.

- Focused on building a personalized financial operating system for micro-entrepreneurs.

🔶 Instantpay

- API-first infrastructure built to power banking and financial services for third-party platforms.

- Offers plug-and-play access to services like AEPS, utility payments, money transfers, and cash withdrawals.

- Scalable middleware connects directly to banks and service providers, enabling real-time transactions.

- Focus on last-mile fintech enablement, powering 10,000+ retail banking points across India.

- Technology stack optimized for high volume, low-latency B2B2C transactions in semi-urban and rural markets.

🏗️ Built to Last: Moats and Differentiators Compared

| Category | Chqbook | Instantpay |

| Target Segment | Urban and semi-urban small business owners, gig workers, and kirana stores | Rural, semi-urban India: agents, retailers, small shops |

| Approach | B2C full-stack digital banking app | B2B2C infrastructure platform with last-mile physical + digital delivery |

| Distribution | The app-first model focused on smartphone users | 10,000+ physical touchpoints via agent network (Digi Marts) |

| Tech Platform | Mobile-led, bundled services, multilingual app | API-first, plug-and-play banking infrastructure |

| Moat (Strength) | Customer stickiness via bundled financial products, high personalization, and underwriting tech | Deep rural penetration, scalable agent infrastructure, strong API rails |

| Compliance & Certifications | Registered Corporate Agent for Insurance; NBFC partnership for lending | NPCI, UIDAI, RBI-compliant tech stack; partners with banks like IndusInd & Axis |

| Product Innovation | Multilingual financial onboarding, Chqbook Score for creditworthiness | Proprietary tech stack for cash logistics, UPI infrastructure for partners |

| Growth Driver | Growing trust in digital tools among self-employed Indians | Demand for assisted digital finance in Bharat (Tier 2/3 towns) |

| Scalability | App-based, dependent on user acquisition and digital adoption | Infra-based, grows as more businesses adopt its APIs and services |

🔍 Key Takeaways:

- Chqbook is focused, app-first, and deeply personalized, ideal for salaried and small business individuals seeking bundled finance.

- Instantpay is infrastructure-first and rural-heavy, enabling financial access for the masses via agents and robust APIs.

- Both solve for SME banking, but Chqbook builds the experience, while Instantpay builds the rails.

✅ Final Verdict: Two Roads to Neobank Scale

India’s SME neo-bank space is no longer a one-size-fits-all game. Instead, it’s a tug-of-war between two bold visions, scale-first infrastructure versus sector-first specialization.

Chqbook, is the bold storyteller. It’s building a financial super-app for India’s gig workers and kirana stores, offering everything from loans and credit cards to insurance, all in one place. It’s an ambitious vision, one that speaks directly to Bharat. While its FY24 financials show stress, the brand still has mindshare and a compelling customer mission. The road ahead hinges on tighter cost control, smarter capital allocation, and stronger monetization, but the opportunity remains massive if it gets those right.

Instantpay , on the other hand is the silent enabler, a fintech infrastructure layer that powers banking services behind the scenes. With over 10,000+ banking points and a robust API ecosystem, it’s designed for scale. It may not be a household name, but its financial discipline speaks volumes. Strong liquidity, lean operations, and better revenue efficiency give it the edge in sustainability. Even as revenues have tapered off from their FY21 peak, Instantpay remains one of the most commercially mature players in this space.

So who wins?

If you’re betting on infrastructure, scale, and efficient cash flow, Instantpay is already ahead.

But if the future belongs to context-driven, community-focused fintech, don’t count Chqbook out yet.

This entire deep dive was made possible by data from PrivateCircle, India’s go-to platform for tracking unlisted companies, startup performance, and real-time financial health.

PrivateCircle helps you discover, compare, and decode the companies shaping India’s next growth wave. From revenue curves to EBITDA trends, shareholding patterns to funding timelines, all in one place.