Kissht (OnEMI Technology Solutions), a digital lending fintech platform, is launching its ₹925.92 Cr IPO. Backed by strong early investors and rapid AUM growth, the company is entering public markets at a time when fintech lending is both high-growth and high-risk.

OnEMI Technology Solutions Limited is a technology-enabled lender in India, primarily offering digital loans through its mobile application for various consumption and business needs.

The company operates under the brand names Kissht (digital lending platform) and Ring (payments app), OnEMI empowers online and offline merchants with seamless consumer credit solutions and EMI-based payments. Its NBFC partner, Si Creva Capital Services, handles loan disbursement, KYC, and EMI collections

As of Dec 31, 2025, the company has 63.73 million registered users and served 11.17 million customers. As of Dec 31, 2025, its AUM stood at Rs 59,557.53 million.

Its product portfolio includes personal loans (offered to salaried and self employed individuals), loan against property, and MSME loans for business expansion and working capital requirements.

But here’s the real twist:

👉 Early investors are already sitting on multi-bagger returns

So, is this IPO a growth opportunity or an exit liquidity event?

Let’s break it down.

IPO Overview

| Particulars | Details |

|---|---|

| IPO Size | ₹925.92 Cr |

| Fresh Issue | ₹850 Cr |

| OFS | ₹75.92 Cr |

| Price Band | ₹162 – ₹171 |

| Lot Size | 87 shares |

| Listing | NSE & BSE |

| IPO Dates | Apr 30 – May 5, 2026 |

Mix of growth capital + partial investor exit

How Kissht Makes Money

KKissht operates as a digital lending NBFC + platform hybrid

Revenue Streams:

- Interest Income

- Personal loans

- Consumer durable financing

- MSME loans

- Processing Fees

- Loan origination charges

- Late Payment Charges

- Penalties on delayed EMIs

- Platform Partnerships

- Merchant integrations & financing tie-ups

👉 Core engine = High-yield unsecured lending

Objectives of the IPO

The proceeds from the IPO are largely intended to strengthen the capital base of its NBFC arm, Si Creva Capital, which in turn will support the expansion of its loan book. The remaining funds will be used for general corporate purposes. In essence, the strategy is straightforward, raise capital, deploy it into lending, grow assets under management, and generate higher interest income.

Investor Exit Analysis

This is where Kissht IPO becomes really interesting 👇

| Investor | Investment (₹Cr) | Value (₹Cr) | Multiple |

|---|---|---|---|

| Vertex Ventures SE Asia & India | 319.74 | 506.49 | 1.6x |

| Ammar Sdn Bhd | 195.23 | 268.27 | 1.4x |

| VentureEast | 49.78 | 209.63 | 4.2x |

| Endiya Partners | 26.31 | 124.21 | 4.7x |

| AION Advisory | 23.43 | 35.26 | 1.5x |

What This Means

- Early investors (2016–2017) → 4x–5x returns

- Late investors (2022) → 1.4x–1.6x returns

- IPO includes OFS → Partial monetisation

This suggests:

- Value creation already happened pre-IPO

- Public investors are entering at a mature stage

Strengths

Kissht benefits from operating in a large and underpenetrated credit market, where many young and first-time borrowers still lack access to formal financing. Its digital-first model allows it to offer quick loan approvals with lower operating costs, making it easier to scale compared to traditional NBFCs.

The company has also shown strong growth in its loan book, reflecting rising customer adoption and expanding reach. Alongside this, improving profitability trends suggest that the business is gradually achieving better operating efficiency.

Additionally, its focus on high-yield unsecured lending supports strong revenue potential per customer, while partnerships with merchants help it acquire users at the point of purchase, strengthening its distribution and growth engine.

Peer Comparison

Based on the RHP, Kissht operates in the digital lending/NBFC segment, with listed peers including Bajaj Finance Limited, SBI Cards and Payment Services Limited, and other consumer lending NBFCs.

| Metrics | Kissht | Bajaj Finance | SBI Cards |

|---|---|---|---|

| Operating Revenue (₹ Cr) | ~1,300+ | 54,000+ | 14,000+ |

| EBITDA Margin | ~20–25% | ~35% | ~30% |

| Profit (₹ Cr) | ~160–200 | 14,000+ | 2,400+ |

| P/E Ratio | ~10.8 | ~30–35 | ~25 |

| Return on Equity | ~12–15% | ~22–25% | ~20% |

Source: RHP, public filings, internal estimates

Kissht operates at a much smaller scale compared to established players like Bajaj Finance and SBI Cards, which highlights the significant gap in size and maturity. While larger peers generate substantially higher revenue and profits, they also benefit from diversified lending portfolios and more stable asset quality.

However, Kissht appears relatively attractive on valuation, trading at a lower P/E multiple compared to peers. This discount reflects the higher risk associated with its unsecured lending model and shorter track record, but it also leaves room for potential upside if the company is able to scale efficiently and maintain credit quality.

👉 Insight:

- Kissht looks cheap vs peers

- But peers have stronger asset quality + track record

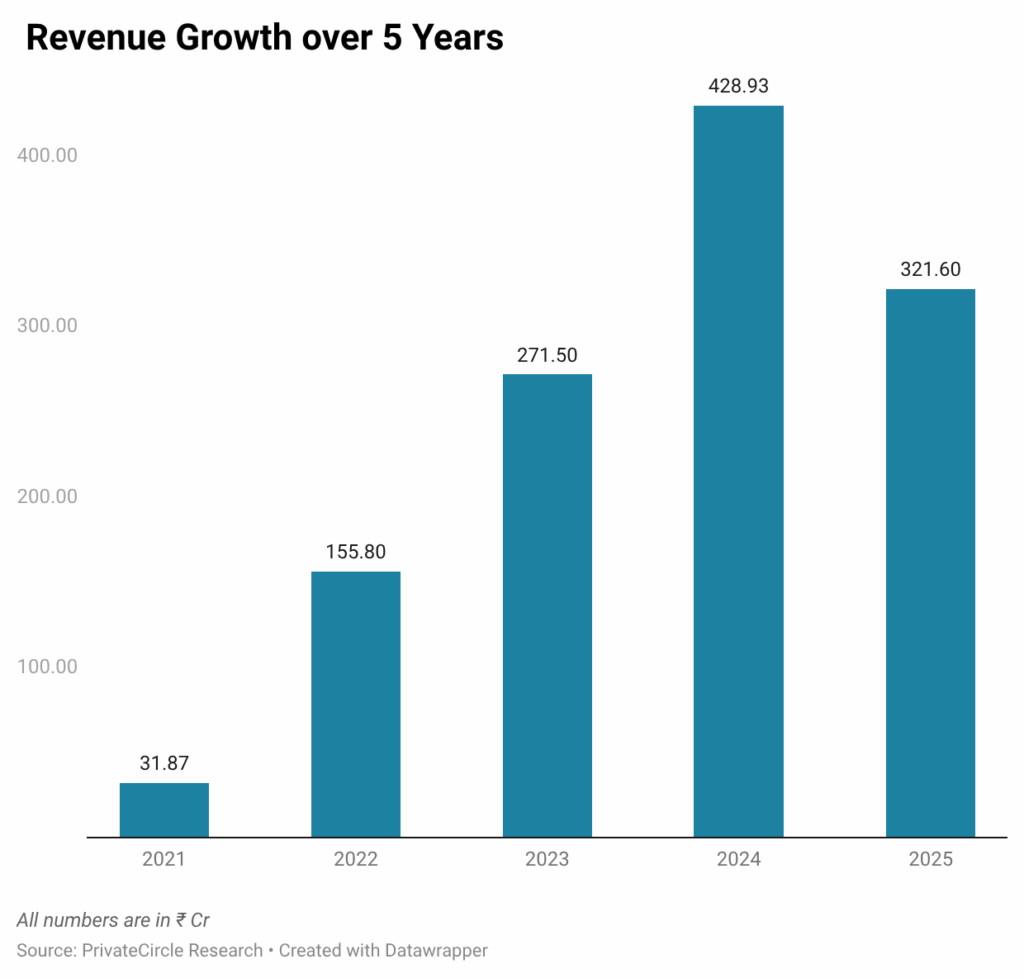

Kissht’s Revenue Growth Over the Last 5 Years

Kissht’s revenue shows a sharp growth trajectory from ₹31.87 Cr in FY21 to a peak of ₹428.93 Cr in FY24, reflecting strong scaling driven by rapid expansion in its loan book and rising customer adoption. This phase highlights the company’s ability to capitalise on India’s growing demand for digital credit.

However, FY25 revenue declined to ₹321.60 Cr, indicating a moderation after a high-growth phase. This could suggest tighter lending practices, credit quality adjustments, or a shift in focus from aggressive growth to more sustainable profitability.

Overall, the trend shows that while Kissht has demonstrated strong scalability, the recent dip signals that the business is entering a more balanced growth phase, where maintaining asset quality and margins becomes as important as expansion.

Who’s Making Money from the IPO?

The most revealing aspect of the Kissht IPO lies in the returns generated by existing investors. Early investors such as VentureEast and Endiya Partners, who entered between 2016 and 2017, have seen their investments grow by over four to nearly five times. In contrast, investors who entered at a later stage in 2022 have recorded more modest returns of around 1.4 to 1.6 times their initial investment.

This indicates that a significant portion of value creation has already occurred before the IPO. While the offer for sale component is relatively small compared to the total issue size, it still represents partial monetisation by investors who have already benefited from the company’s growth journey.

For public market investors, this means entering at a stage where future returns will depend more on sustained execution rather than early-stage expansion.

Final Thought

Kissht’s IPO reflects a classic transition from private to public markets, where early investors have already captured substantial gains and new investors are betting on the company’s ability to scale further. The opportunity lies in its exposure to India’s growing digital credit ecosystem, but the risk lies in maintaining credit quality and navigating regulatory challenges.

Ultimately, this is not just a growth story, but a test of whether Kissht can convert rapid expansion into consistent and sustainable profitability over the long term.

For deeper IPO breakdowns and investor-level insights, PrivateCircle keeps you ahead.