India’s fintech ecosystem has undergone a radical transformation in the past decade. As traditional banks grapple with legacy systems, high documentation requirements, and a preference for prime customers, millions of underserved and new-to-credit users have been left behind. This vacuum has been quickly filled by nimble digital lending startups that use technology to assess, approve, and disburse loans within minutes.

According to industry estimates, the digital lending market in India is expected to cross $1.3 trillion by 2030, and startups like Fibe and KreditBee are poised to capture a significant share. These two companies exemplify how diverse approaches can thrive in the same sector: one focusing on salaried professionals (Fibe), and the other on new-to-credit youth and gig workers (KreditBee).

Founders & Origin Stories

Fibe:

Fibe, formerly known as EarlySalary, was founded by Akshay Mehrotra and Ashish Goyal. Akshay, an IIM Lucknow graduate and ex-CMO at PolicyBazaar, brought marketing and fintech DNA, while Ashish added strong capital markets and technology experience. They realized that young working professionals often needed access to instant credit for emergencies or aspirations, but were underserved by banks.

Starting with salary advances, the company gradually evolved into a full-stack consumer lending platform that now offers personal loans, lifestyle BNPL products, and credit lines in sectors like healthcare, education, and wellness.

KreditBee:

KreditBee, operated by Finnovation Tech Solutions Private Limited, was founded by Madhusudan Ekambaram and Karthikeyan Krishnaswamy. Madhusudan, previously at ICICI Bank and Flipkart, envisioned a platform that could provide first-time borrowers with fast, accessible credit using only their mobile phones. Karthikeyan added deep tech capabilities.

Their approach was more experimental from day one: start with small-ticket loans, build repayment history, and then upsell longer-tenure products. With the backing of Finnov Pte Ltd and an in-house NBFC (Krazybee Services), KreditBee became known for serving the “Bharat” segment with instant, easy-to-access loans.

Business Models

Fibe:

Fibe operates a hybrid lending model:

- In-house lending through its NBFC arm to retain margin and control risk

- Co-lending partnerships with banks and NBFCs to scale without bloating its balance sheet

- Distribution-led revenues from cross-selling financial products

The company earns from:

- Interest income on loans

- Processing & convenience fees

- Recurring revenue from partnerships in sectors like healthcare & edtech (BNPL)

This gives Fibe the flexibility to scale while ensuring unit economics remain favorable. Its salary-based approach also ensures lower NPAs and high renewal rates.

KreditBee:

KreditBee’s model is built on speed, scale, and partnerships:

- Lending via Krazybee is a systemically important NBFC

- Partnering with over 10 NBFCs and financial institutions

- A technology platform that monetizes via loan origination, servicing fees, and credit add-ons

Key monetization streams include:

- Interest spread on own book

- Platform fees on partner disbursals

- Ancillary services (e.g., credit insurance, delay penalties)

This model allows KreditBee to scale rapidly without significantly expanding its loan book while maintaining agile user onboarding.

Product Offerings

| Product Type | Fibe (EarlySalary) | KreditBee |

| Instant Loans | Yes (as low as ₹8,000) | Yes (as low as ₹6,000) |

| Personal Loans | Up to ₹5 lakhs for salaried users | Up to ₹10 lakhs for broader segments |

| BNPL Products | Health, edtech, e-commerce partnerships | E-commerce + merchant checkout BNPL |

| Credit Line | Limited; prefers fixed-term PLs | Strong focus on flexible credit line |

| Insurance Add-ons | Yes, in collaboration with partners | Yes, bundled with loans |

| Other Services | Credit score checks, EMI calculators | Credit protection plans |

Both platforms have diversified their offerings, but Fibe leans toward lifestyle and sectoral financing while KreditBee focuses on mass-market cash flow credit.

Lending Strategy

Fibe:

- Target Group: Salaried millennials in Tier 1/2 cities

- Loan Tenure: 6–36 months

- Repeat Usage: High, especially for personal loans

- Risk Controls: Deep integration with employer databases, use of CIBIL, Equifax, and bureau data

- Collections: Combination of auto-debit, call center follow-up, and in-app reminders

KreditBee:

- Target Group: First-time borrowers, gig workers, youth

- Loan Tenure: 6–60 months

- Repeat Usage: Very high; many users take loans monthly

- Risk Controls: AI-led alternative underwriting using mobile metadata, SMS reading, and device behavior

- Collections: App reminders, call centers, and field agents (for large defaults)

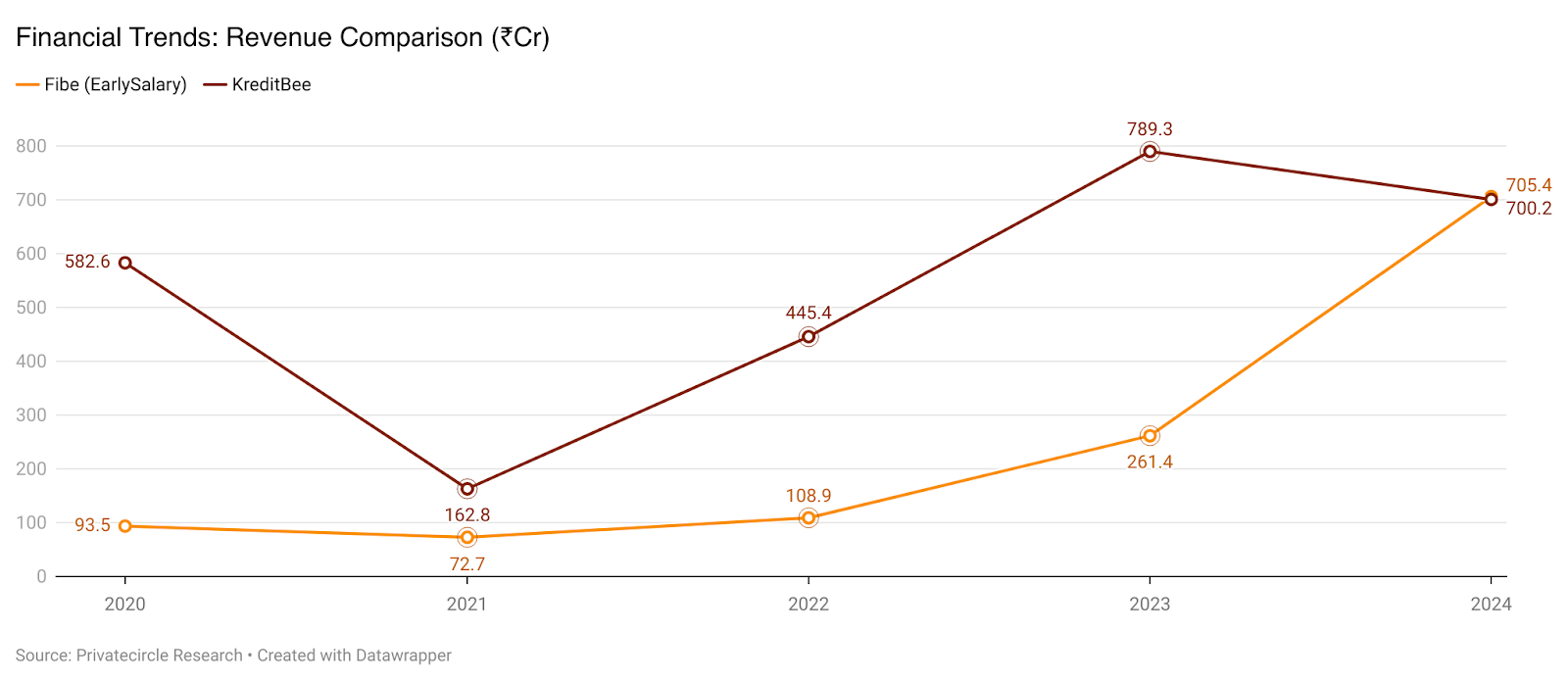

Financial Trends: Revenue Comparison (₹Cr)

Key Insights:

- Fibe’s revenue grew 7.5x from FY20 to FY24

- KreditBee peaked in FY23 and stabilized in FY24

- Fibe is catching up despite starting lower

Investor Base

Fibe:

Fibe (Earlysalary Services Private Limited) functions under the parent company, Social Worth Technologies Private Limited, which serves as the operating backbone for its digital lending business. Over the years, it has garnered the support of some of the most respected names in venture capital, including Chiratae Ventures, The Rise Fund (TPG), Eight Roads Ventures, and Norwest Venture Partners. These investors have helped fuel Fibe’s growth into a trusted name in consumer lending. As of July 2024, the company is valued at approximately ₹1,641 crore.

KreditBee:

KreditBee operates under the broader corporate umbrella of Finnov Pte Ltd, a Singapore-based holding company. Its registered lending arm in India, Krazybee Services Private Limited, is a systemically important NBFC, giving it a regulated base to scale credit offerings. KreditBee has attracted investments from reputed institutional backers such as PremjiInvest, MUFG Bank, Mirae Asset, and Motilal Oswal Private Equity. These investors support its mass-market lending strategy and technology-led growth engine. As of March 2024, KreditBee was last valued at approximately ₹1,425 crore.

Tech Stack & Differentiation

Fibe:

- Tech Platform: Proprietary app (Android/iOS)

- Risk Engine: AI/ML + bureau + employment data

- Collections Tech: Reminder bots, email, NACH

- Partner APIs: Hospitals, edtech, e-commerce platforms

KreditBee:

- Tech Stack: Java-based backend, Android-first

- Alternative Data: Device metadata, app installs, SMS patterns

- AI Models: Cluster-based segmentation for renewals

- Scalability: Handles 10+ lenders via one pipe

Competitive Moats & Risks

| Factor | Fibe | KreditBee |

| Regulatory Status | NBFC + RBI compliant | Systemically Important NBFC (Krazybee) |

| Risk Management | Bureau + income underwriting | Alternative data + AI models |

| Revenue Diversity | Loans + BNPL + partners | Primarily loans |

| Default Risk | Lower (salaried base) | Higher (NCT segment) |

| Scalability | High via partners | High via embedded APIs |

| Vulnerabilities | Credit tightening, partner risk | High NPAs, regulatory scrutiny |

Who Will Scale Smarter?

Strategically speaking:

- Fibe is better poised for premium partnerships, stronger regulation alignment, and higher lifetime customer value through embedded finance.

- KreditBee is optimized for mass-market access, hyper-growth, and speed, making it resilient in high-volume, fast-turnaround environments.

Challenges:

- Fibe must carefully manage its operational scale as it integrates with multiple verticals (BNPL, wellness, edtech).

- KreditBee faces potential regulatory scrutiny and credit risk volatility due to its high exposure to NTC (new-to-credit) segments.

Who will scale smarter? It’s not a binary outcome.

- In a scenario where the RBI tightens norms, platforms like Fibe will likely benefit from their structured compliance.

- In an expanding consumption credit market, KreditBee’s speed and user acquisition engine will win.

Ultimately, both players are indispensable to the broader vision of financial inclusion in India, each fulfilling a distinct demand:

- Fibe is building a durable, trust-led financial institution.

- KreditBee is creating the rails for India’s next 500 million borrowers.

The winners in Indian fintech will not just be those who scale fast, but those who scale sustainably, compliantly, and intelligently. And both Fibe and KreditBee, in their ways, are making that possible.

Fibe and KreditBee are both solving real credit pain points in India, but they’re doing it differently:

- Fibe is a trust-first lender focused on professional stability. Its tech + compliance playbook may allow it to become India’s next big embedded finance player.

- KreditBee is a velocity-first model optimized for Bharat. It wins in new-to-credit access and monetization through renewals.

Verdict:

- For long-term asset quality and BNPL ecosystem leadership, Fibe looks promising.

- For scale, user acquisition, and monetizing first-time borrowers, KreditBee is hard to beat.

In a market as large and fragmented as India, there may not be one winner, only different champions for different credit needs.

Conclusion

Fibe and KreditBee represent two distinctly successful models in India’s booming digital lending ecosystem. Though both companies entered the digital lending space in their early growth phases, they have since taken distinctly divergent paths to achieve scale, traction, and sustainability in the Indian credit market.

Fibe, with its roots in the salaried working class, has built a platform that emphasizes credit reliability, financial discipline, and compliance-first scaling. Its hybrid lending model, reliance on bureau data, and partnerships with hospitals, edtechs, and enterprises reflect a strategy built on trust and recurring behavior. Fibe has made strong inroads with the aspiring urban middle class, and its emphasis on longer-tenure personal loans, embedded BNPL, and financial wellness tools positions it well for long-term profitability. Its revenue has grown nearly 7.5x in five years, signaling operational excellence and strong user retention. Moreover, Fibe’s broader institutional investor backing (including Chiratae Ventures, Eight Roads, and Norwest) gives it a strategic advantage in credibility, capital access, and regulatory trust.

On the other hand, KreditBee is a masterclass in velocity, accessibility, and monetization at scale. Designed for India’s credit-starved youth and gig workers, it has built a reputation for speed, both in disbursal and renewals. KreditBee’s use of alternative underwriting data (like mobile metadata and app usage) enables it to serve segments where traditional credit systems fail. Its average loan is smaller, but its repeat cycles are faster. By operating through Krazybee (its NBFC) and layering in multiple partners, KreditBee scales efficiently without burdening its balance sheet. While the risk is naturally higher in this segment, its tech-first collection architecture and AI-based risk segmentation give it defensibility. KreditBee’s platform is built for volume-driven profitability, and its scale in first-time borrowers is unmatched.

Powered by PrivateCircle, your trusted source for private company financials, valuations, and fundraising insights. Stay ahead with verified, MCA-synced intelligence.