A Deep-Dive Into India’s Fastest-Scaling Digital Lender for Small Businesses

Why SME Lending Matters

Small and Medium Enterprises (SMEs) are the backbone of India’s economy. They contribute over 30% to the GDP and account for nearly half of the country’s exports. Yet, they remain vastly underserved when it comes to credit access.

According to the Reserve Bank of India, the SME sector faces a massive credit gap of over ₹25 lakh crore. Traditional banks are often reluctant to lend to these businesses due to perceived high risks, lack of collateral, and incomplete financial documentation.

That’s where Capital Float now known as Axio steps in.

Axio is a digital-first NBFC that combines fintech innovation with strong banking partnerships. It offers fast, flexible, and unsecured loans tailored for small businesses. Over the years, the company has also expanded into BNPL and consumer lending, but its core mission remains focused on solving the credit needs of Indian SMEs.

Digital-First, Co-Lending Backed, Zero CAC

🔹 NBFC Backbone + Embedded Platform

Axio operates under an NBFC license, allowing it to lend from its balance sheet and participate in co-lending structures. It runs a digital origination engine, has no physical branches, and no paper trails. Borrowers apply through embedded partners (like Amazon, POS terminals, e-commerce checkouts), and the entire journey from application to disbursal is digitized.

🔹 Co-Lending Model

Axio doesn’t fund most loans alone. Instead, it teams up with regulated banks and NBFCs:

- Axio underwrites and originates the borrower.

- Typically, Axio funds 20%, while the partner bank contributes 80%.

- Risk and return are shared, enabling scale without balance sheet stress.

This lets banks meet Priority Sector Lending (PSL) targets efficiently while Axio retains a leaner balance sheet.

🔹 Zero CAC Flywheel

Customer acquisition is often the Achilles’ heel of lending. But Axio turned this around by embedding itself into merchant platforms:

- E.g., Amazon bears the marketing and customer acquisition costs.

- In return, Axio pays a subvention fee or shares interest revenue.

This keeps CAC at near zero, making lending more profitable, even at small ticket sizes.

Tailored Credit for Every Segment

👨💼 SME-Focused Credit Products

🔸 Working Capital Loans

Short-term business loans ranging from ₹5–50 lakh with 6–36 months tenure. These are collateral-free, with quick approvals based on cash flows, GST data, and transaction history. Ideal for small manufacturers, traders, and service providers needing liquidity.

🔸 Merchant Cash Advance

This unique offering ties loan repayment to POS terminal activity. For example, if a kirana store swipes ₹2 lakh/month, Axio might advance ₹4–5 lakh, repaid via a 10% daily deduction from sales.

🔸 School Finance Loans

Offered to small schools or educational institutes, this niche segment often lacks credit access but has predictable fee-based cash flows. Ticket size ranges from ₹5 to ₹50 lakh.

🛍️ Consumer-Focused Credit Products

🔸 BNPL – Amazon Pay Later & Checkout Credit

In partnership with Amazon, Axio powers Pay Later at checkout. Initial limits range from ₹10,000–₹25,000, with repayment in 3–12 EMIs. Successful usage upgrades customers to higher limits and personal loans.

🔸 Personal Loans (Top-Up for BNPL Users)

Users with strong BNPL repayment behavior get access to longer-term loans (₹25K–₹3 lakh). These loans often come with 6–36 month tenure, and are fully financed on Axio’s NBFC books.

🔸 Checkout Finance with Razorpay, Decathlon, Xiaomi

These merchant tie-ups allow Axio to offer embedded credit for purchases, e.g., smartphone EMIs via Xiaomi or sports gear on Decathlon.

The Engine Behind Axio’s Growth

🔹 Distribution Partners

Axio’s scale isn’t just tech, it’s partnerships.

- Amazon India: Accounts for ~50–60% of disbursements. Axio provides BNPL to Amazon shoppers and taps seller data for SME underwriting.

- Razorpay: Lets small merchants access working capital via payment history.

- Xiaomi, Decathlon, Policybazaar: Embedded EMI and checkout credit.

- Pine Labs & POS Vendors: Allow access to offline merchant data for MCA products.

These integrations allow Axio to underwrite loans using real transactional data, a competitive edge over traditional lenders.

🔹 Co-Lending & Banking Partners

- Banks like RBL, IDFC First, and Tata Capital co-lend with Axio.

- These relationships bring scale, compliance, and interest rate advantage.

- Co-lending also ensures risk diversification.

🔹 Investors and Strategic Backers

- Raised over ₹1418 Cr equity and ₹701 Cr debt to date.

- Key investors: Sequoia (Peak XV), Ribbit Capital, Elevation Capital, Amazon, Creation Investments.

- Amazon’s acquisition deal in late 2024 positions Axio as a strategic long-term fintech play within Amazon’s India stack.

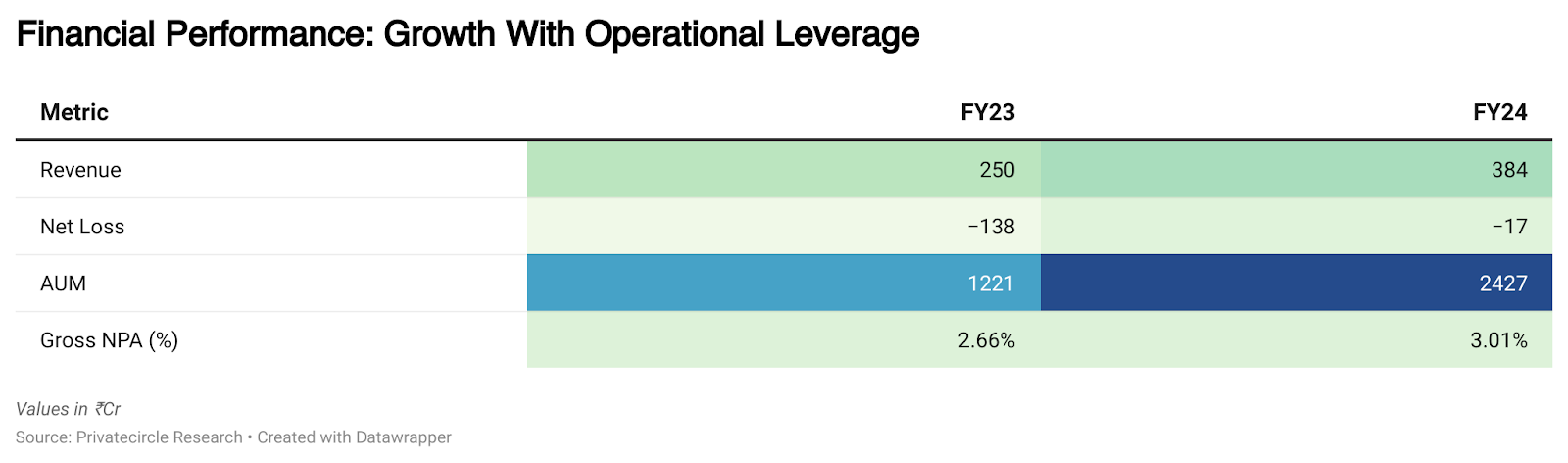

Growth With Operational Leverage (₹Cr)

Key Insights:

- Revenue surged by 53% YoY, showcasing Axio’s ability to scale both SME and BNPL offerings in tandem.

- Net loss narrowed sharply to just ₹17 Cr in FY24, signaling a potential shift toward full-year profitability.

- AUM doubled within a year, indicating strong traction in both SME lending and consumer credit.

- GNPA remained stable, slightly increasing to 3.01%, a healthy figure for unsecured digital lending, reflecting disciplined underwriting..

Navigating India’s Fragmented Lending Arena

India’s lending ecosystem, especially in the SME and consumer segments, is intensely competitive, with fintechs, NBFCs, and banks all vying for market share. Axio stands at the intersection of multiple competitive battlegrounds, each with its own dynamics and challenges.

🏦 A. SME Lending Segment

Peer Set:

- Lendingkart – Among the earliest digital SME lenders; strong analytics-led underwriting, but higher NPAs.

- NeoGrowth – Focused on POS-based lending, much like Axio’s MCA product.

- Flexiloans & Indifi – Marketplace models with pure tech underwriting; more reliant on anchor partners.

- Aye Finance – Strong rural outreach, but operates through physical branches.

Axio’s Distinct Edge:

- ⚡ Embedded origination via e-commerce: Unlike others who rely on inbound or DSA channels, Axio gets leads directly from partner platforms (Amazon, Razorpay).

- 💼 Co-lending infrastructure: Many rivals operate solely from their own NBFC books, while Axio uses risk-sharing with banks, giving it capital efficiency.

- 📉 Lower customer acquisition cost: Thanks to subvention-led acquisition by platforms like Amazon.

Challenges:

- Some competitors like Aye or Lendingkart have deeper presence in rural clusters and longer operating history in specific verticals (e.g., manufacturing clusters).

- Banks are improving their SME tech stacks and catching up on credit analytics.

💳 B. BNPL & Consumer Lending Segment

Peer Set:

- ZestMoney – Early mover in BNPL, recently facing regulatory and funding headwinds.

- LazyPay (PayU) – Popular with Gen Z/millennials for small-ticket loans; wide merchant base.

- Simpl, Slice, OneCard – New-age credit products focused on lifestyle and convenience.

- Traditional Banks – Now launching their own BNPL and card-based EMI programs, e.g., ICICI PayLater.

Axio’s Strengths:

- 🛒 Exclusive partnership with Amazon Pay Later – Arguably the widest BNPL channel in India (~50–60% of Axio’s disbursals).

- 🔐 NBFC license – Unlike many BNPL peers that rely on bank partnerships, Axio directly lends and controls risk end-to-end.

- 🧠 Data loop from BNPL to personal loans – It upgrades good BNPL borrowers to high-ticket personal loans, creating a credit lifecycle journey.

Challenges:

- BNPL is becoming commoditized, with thinner margins and rising delinquencies.

- RBI’s scrutiny over digital lending and credit bureaus’ pushback on thin-file lending could lead to compliance risks or a growth slowdown.

Scaling with Conviction

The next few years could be transformative for Axio. With fundamentals improving and strong backing from investors (and potentially Amazon), the company is poised to scale not just in size, but in strategic relevance within India’s credit infrastructure.

🚀 A. Amazon Acquisition: Game-Changer in the Making

Amazon is currently in the final stages of acquiring Axio. If the RBI approves the deal, it could create a precedent in Indian financial regulation, where a global tech giant holds an NBFC license.

What This Means:

- 🔗 Deeper platform integration: Axio’s credit stack could become the default credit engine across Amazon Pay, seller loans, Prime Day financing, and more.

- 📈 Demand-side explosion: With access to millions of active Amazon users and sellers, Axio could double its monthly origination volumes without incremental CAC.

- 🌏 Global playbook: If successful, this could be Amazon’s model for digital credit across other emerging markets.

🌐 B. Expanding the SME Lending Flywheel

While BNPL has driven near-term growth, Axio’s long-term brand moat will come from solving credit access for underserved small businesses.

Strategic Goals:

- 🧱 Deeper Tier 2/3 city coverage: Focus on low-NPA geographies with rising formalization (e.g., Indore, Coimbatore, Bhubaneswar).

- 📊 New product lines: Invoice discounting, supply chain finance, revenue-based lending for D2C brands.

- 💰 PSU Bank partnerships: Explore tie-ups with SBI, BoB under co-lending to reduce the cost of capital further.

- 🧾 Cross-sell insurance & gold loans: Leverage the consumer loan base for wallet share monetization.

📊 C. IPO Potential: Building a Profitable Fintech Narrative

If Axio maintains current revenue growth and turns fully profitable in FY25, it could be IPO-ready by FY26–27. Its diversified credit engine, embedded distribution model, and bank partnerships make it a strong story for public markets.

Key Metrics to Watch:

- EBITDA breakeven & PAT turnaround

- Asset quality stability (GNPA below 3%)

- Equity raise vs. debt leverage

- Regulatory clarity on Amazon-led NBFCs

From Startups to SMEs, A Fintech Story That Matters

Axio has emerged as one of India’s most efficient SME credit engines. While its consumer arm (BNPL, personal loans) has helped it scale rapidly, the company’s core DNA remains SME-first.

Its low-CAC model, real-time underwriting, bank partnerships, and embedded channels form a defensible moat. If it maintains credit discipline and scales co-lending wisely, Axio could become India’s most successful full-stack lending platform, one that empowers the “missing middle” of India’s business economy.

All insights in this report are sourced via PrivateCircle, the most trusted platform for private company financials and ecosystem intelligence.